Contract Savings for Housing (CSH), Insurance, high-LTV Lending

In my career I have diagnosed and developed all major instruments and institutions that provide access to credit in housing finance.

At the consulting firm empirica in the 1990s I covered all aspects of German Bausparen (contract savings for housing, CSH), a system that was originally developed in Britain and revived in Germany in the 1920s in response to high inflation and inability of capital markets and banks to provide individual housing finance. A key focus of my work then was detailed household survey analysis focusing on understanding savings behavior and capital formation dynamics.

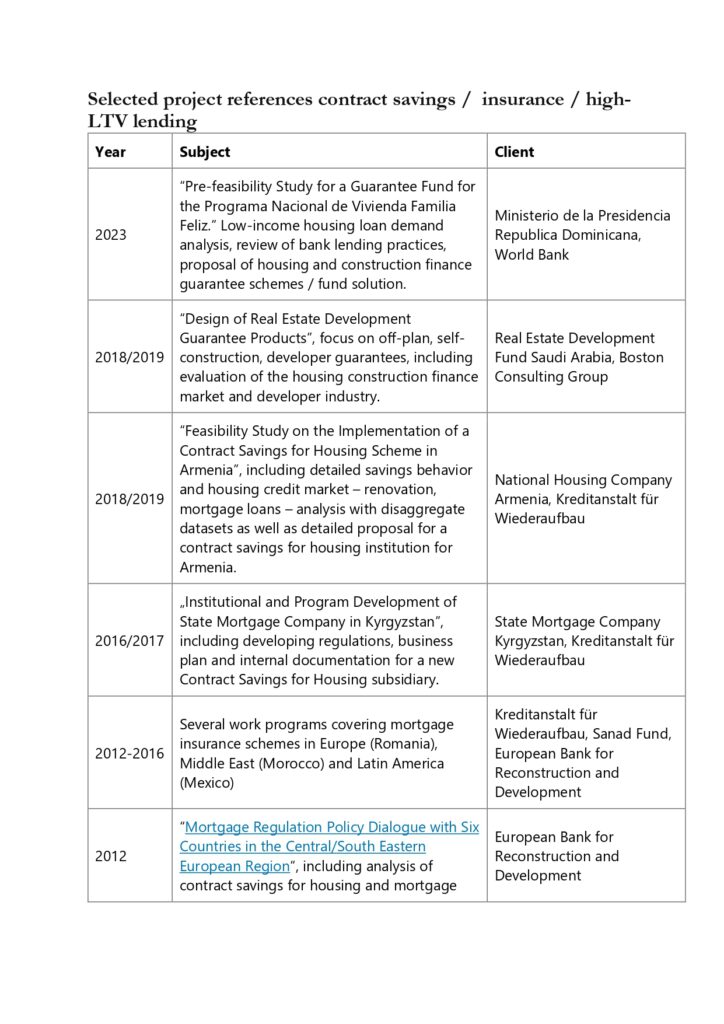

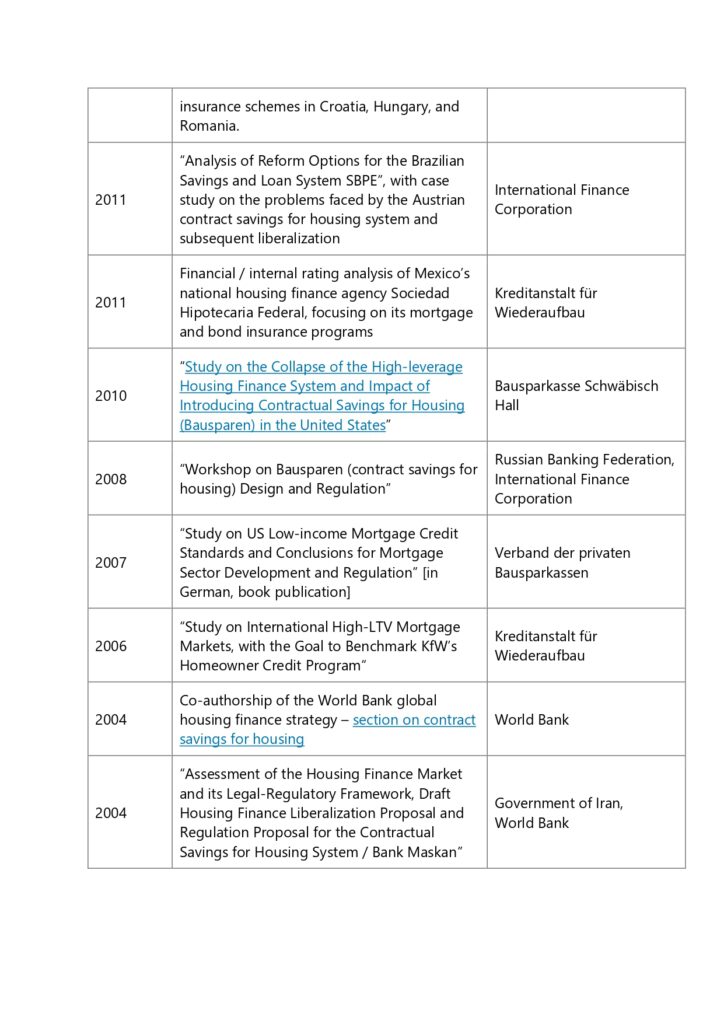

From the mid-1990s onwards I became involved in the debate over introducing contract savings for housing in transition countries, where the ‘German’ view that building equity through savings prior to taking out a mortgage loan was essential to stability and capital formation collided with the ‘American’ view that high-LTV mortgage insurance was suited to create an automatic equity accumulation mechanism through capital gains. The ‘American’ view died a sudden death in the GFC, which prompted me to write a critique of the U.S. high-LTV (insurance) system together with a proposal to introduce contract savings in the U.S. in 2010. Needless to say that America nevertheless ‘rescued’ the high-LTV insurance system – through regulatory forbearance and the sheer political force of Fannie / Freddie, which reminds of Churchill’s quip that the country ‘will always do the right thing after having explored all alternatives’ (i.e., maybe after the next crisis).

Many transition countries without the deep financial coffers of the U.S. latest with the ensuing foreign currency lending (i.e., capital market) crisis from 2009 onwards were either happy to have built a CSH system already (such as Hungary or Kazakhstan) or started creating one. From 2016 onwards I helped developing the CSH institution that has taken up business in 2020 in Kyrgyzstan and in 2019 developed a feasibility assessment and an implementation plan for a second-tier institution run by the central bank in Armenia.

For sure, CSH institutions may be tricky to sustain under high inflation and heavy policy intervention, which explains my 2004 work in Iran with World Bank trying to reform the failing Bank Maskan. A less dramatic, but still unsatisfactory, case is the Brazilian SBPE savings bank system that left the platform of voluntary CSH and became directed credit system with all its inefficiencies and on which I have worked repeatedly since 2000. Emerging markets are still full of such mandatory savings for housing institutions that are difficult to reform once the recipients of the liquidity are getting used to cheap sources of funding. An issue can also be excessive subsidization.

Despite its systemic failure in managing cyclical property price risk through pushing leverage and frequent regulatory arbitrage character, I am convinced that insurance has its firm place as an access to credit and system risk management product in housing finance. Insurance in real estate has value in particular when designed to improve the efficiency of developer / project / idiosyncratic borrower credit risk management across the banking sector, especially if combined with crisis resolution and catastrophic risk backup mechanisms. In 2023 I proposed a menu of guarantee schemes in retail mortgage and construction finance for the Dominican Republic. Innovative parts included a cash flow guarantee facilitating pre-foreclosure interaction between lenders and defaulting borrowers, and a guarantee scheme enabling high loan-to-cost lending to SME developers. I helped develop the product menu of Saudi Arabia’s REDF agency in 2018/19 regarding developer loan and related project finance guarantees for new builds, which tried to help the ambitious mass off-plan housing program proposed take off through a credible backup mechanism for the fragmented and undercapitalized developer industry. Well managed insurers, such as SHF in Mexico whose performance in Mexico I diagnosed in 2013 when it was heavily tested after the GFC, constantly adjust their instrument focus and design to put their capital to optimal use. Unfortunately, many public insurers are as heavily politicized as mandatory contract savings institutions, as a World Bank team that included myself experienced during our work in the late 1990s on the Philippines where the insurer essentially sold regulatory capital favors and never saw a call on its guarantees.

Despite the mixed empirical picture I believe that between CSH and insurance , also including lender self-insurance, in this complex and extremely difficult to calibrate market segment there are a few instruments and institutional models that can indeed serve housing and mortgage policy makers as templates. Key to success is a sound financial and risk analysis, as well as an open mindset of both advisor and client to what could work best in the given circumstances.

Selected presentations and papers contract savings / insurance / high-LTV lending

“Contract Savings for Housing, A Window of Opportunity?” European Federation of Building Societies, Prague, October 2019.

“Integration of Pension and Housing Savings – a Conceptual Discussion“, Paper resulting from consulting activities with National Housing Company of Armenia / Kreditanstalt für Wiederaufbau, March 2019.

“Lessons from Introducing Contractual Savings for Housing Schemes in Transition Countries“, Paper resulting from consulting activities with National Housing Company of Armenia / Kreditanstalt für Wiederaufbau, March 2019.

“Mortgage Capital Market and Access to Credit Instruments with special focus on Covered Bonds and Contract Savings for Housing“, Workshop held at the National Bank of Georgia, June 2018.

“Contract Savings for Housing for Kyrgyzstan“, Workshop held at the State Mortgage Company, April 2017.

To be continued.